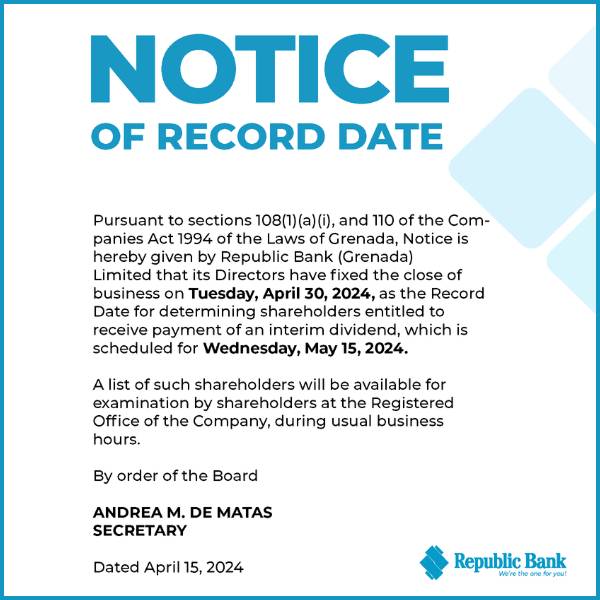

The National Insurance Scheme (NIS) contribution rate will increase gradually each year until it reaches 16% in 2031.

As always, the contribution will be split between the employee and the employer:

| Year of Increase | Employer Increase % | Employee Increase % | New Contribution Rate % |

| 2023 | 0.5 | 0.5 | 12.0 |

| 2024 | 0.25 | 0.25 | 12.5 |

| 2025 | 0.25 | 0.25 | 13.0 |

| 2026 | 0.25 | 0.25 | 13.5 |

| 2027 | 0.25 | 0.25 | 14.0 |

| 2028 | 0.25 | 0.25 | 14.5 |

| 2029 | 0.25 | 0.25 | 15.0 |

| 2030 | 0.25 | 0.25 | 15.5 |

| 2031 | 0.25 | 0.25 | 16.0 |

The total contribution payment must be remitted to the NIS at the end of each month. The National Insurance Laws allow for a grace period of 14 days from the end of the month within which contributions must be paid. Employers failing to do so will be charged a 10% surcharge and an additional 1% interest for every month or part of a month that the contribution payment remains outstanding.

NOW Grenada is not responsible for the opinions, statements or media content presented by contributors. In case of abuse, click here to report.